Mobility industry disruption is happening; many will be impacted

Today is the Slowest It is Going to Be

London-based

Lauri Murphy, GMS-T

TAIN Management Consulting

Disruptive Strategy & Applying Innovation Theory –Harvard Business School

New York-based

SUSAN GINSBERG

Founder, Managing Principal

SRG ADVISORY aligns a company’s vision with a changing world.

Revenue growth occurs by identifying and leveraging new opportunities, new markets, new customers.

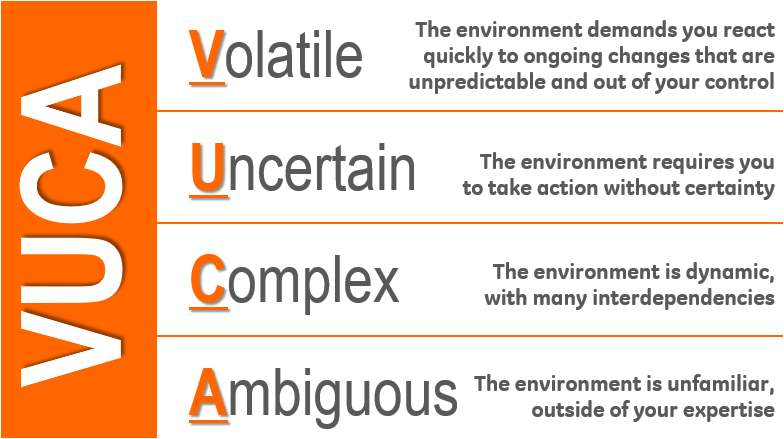

VUCA:

Volatile, Uncertain, Complex, Ambiguous.

It was coined by the US Army College in the late 1980s as they grappled with a new reality as the Berlin Wall came down and communism in Europe came to an end. They were looking to understand what type of world they would be operating in as they approached the 21st century.

Nowadays, the concept of VUCA is now deeply embedded into corporate life. The impact of the Trump presidency, Brexit, and the current concerns around coronavirus (COVID-19) all point towards a more precarious social, political and economic climate. (COVID-19) has already created significant upheaval in financial markets with the OECD warning the virus presents the biggest threat to the global economy since 2008.

Amazon & Netflix

A report by Credit Swiss in 2017 predicted that 20% to 25% of shopping malls will close between 2017 and 2023. I know from living in London, walking up any typical high street in the capital, I am struck by the number of charity shops and cafes that have replaced more traditional shops. The decimation of retail is The Amazon Effect. In the U.S., we sadly see fewer local boutiques, as many have been replaced by corporate organisations that can manage locals with high foot traffic.

Netflix, which started out as a DVD rental player, has not only revolutionised the way we watch TV but also how we spend disposable time. Netflix saw off Blockbusters at a time when it was far and away the market leader and seemingly untouchable. The Netflix impact is also putting the BBC’s business model under extreme pressure, as the younger generation questions whether they should pay a license fee for a service they barely use, if at all.

Brave new world

Now if we now flip over to the global mobility/relocation industry and ask what the future could look like; it is foolhardy to predict it with any degree of certainty. What we can say is it is an industry going through huge disruption.

The corporate global mobility professional currently has a focus on somewhere between 1% and 3% of the workforce. If we include frequent business travellers, this may see it rise but still within single digits. This is coupled with the demographic shift in the workplace and different type of movers all points to significant change for the role itself. For example, many millennials typically don’t own their own home or have accumulated the amount of worldly household goods of other generations. Therefore, they are more likely to rent furniture from IKEA or another rental provider when they move.

Corporations and the mobility function are also seeing a host of other move types that will reduce the number of traditional long-term assignments (LTA), with short term assignments, commuters type moves popular in Europe and frequent business travel. These move types, alongside one-way permanent moves, are all looking to be a more cost-effective way of getting people where the company needs them.

Survival of the fittest

What does all this mean for some of the key service providers in the industry? Relocation Management Companies (RMCs) have seen their traditional cash-cows, US home sale and LTA, go into somewhat of a decline. Traditional business models for RMCs are not sustainable; revenue from referral programmes, which do not add any value beyond financial reward, are also coming under more scrutiny.

Furthermore, with procurement playing a more influential role than ever and a focus on cost like never before, it begs the question: where do key mobility providers, especially RMCs, go from here? How do they differentiate themselves? How do they achieve their own business growth?

A recent survey by Alan Trippel saw over 20 companies identifying themselves as RMCs. On examining many industries there are typically a smaller number of dominant players and certainly fewer than 20. Further consolidation is inevitable as we wait and see how BGRS and others might respond to the SIRVA/Cartus deal. The result may then create more space for Tier II RMCs.

As technological innovations continue to enter the industry at a fast rate, DSPs are the next level of service providers that offer key services to assignees and their families on the ground, across the globe, many of whom work with RMCs as well as have their own client portfolio. These service providers are also coming under pressure as they are asked to do more with less in the face of shrinking margins.

Ultimately, we don’t yet know whether the future will belong to an Amazon-type player that will come to dominate the mobility industry for years to come. Or if there will be a smaller number of key players serving the changing mobility needs of the population, while offering others the space to carve out their own niche as the landscape continually evolves.

What we can say with some degree of certainty is that Companies that differentiate themselves in a changing, shrinking landscape and establish an innovation roadmap will grow.

Being collaborative, agile and consultative are vital to delivering successful outcomes.

The need to move talent is still a real and necessary business imperative.

Service organisations that adapt will thrive.

Susan Ginsberg is based in New York; Founder, Managing Principal -SRG Advisory.

Lauri Murphy is based in London and works as MD with TAIN Consulting Ltd.

Both are trusted partners to corporate HR/Mobility Leaders as well as to industry service providers.